North Carolina Promissory Note Templates

A promissory note is a legally binding loan agreement that two people can fill out without lawyers. These notes describe who partook in the loan, how much money exchanged hands, when the borrower must repay the loan, and what sort of penalties exist should the borrower default on the loan.

The maximum interest rate for a North Carolina promissory note is 8%, according to North Carolina General Provisions § 24-1. There’s little legal jargon to sift through, and many websites offer a free North Carolina promissory note template, so laypeople can access one easily.

There are two types of promissory notes in this state: secured and unsecured.

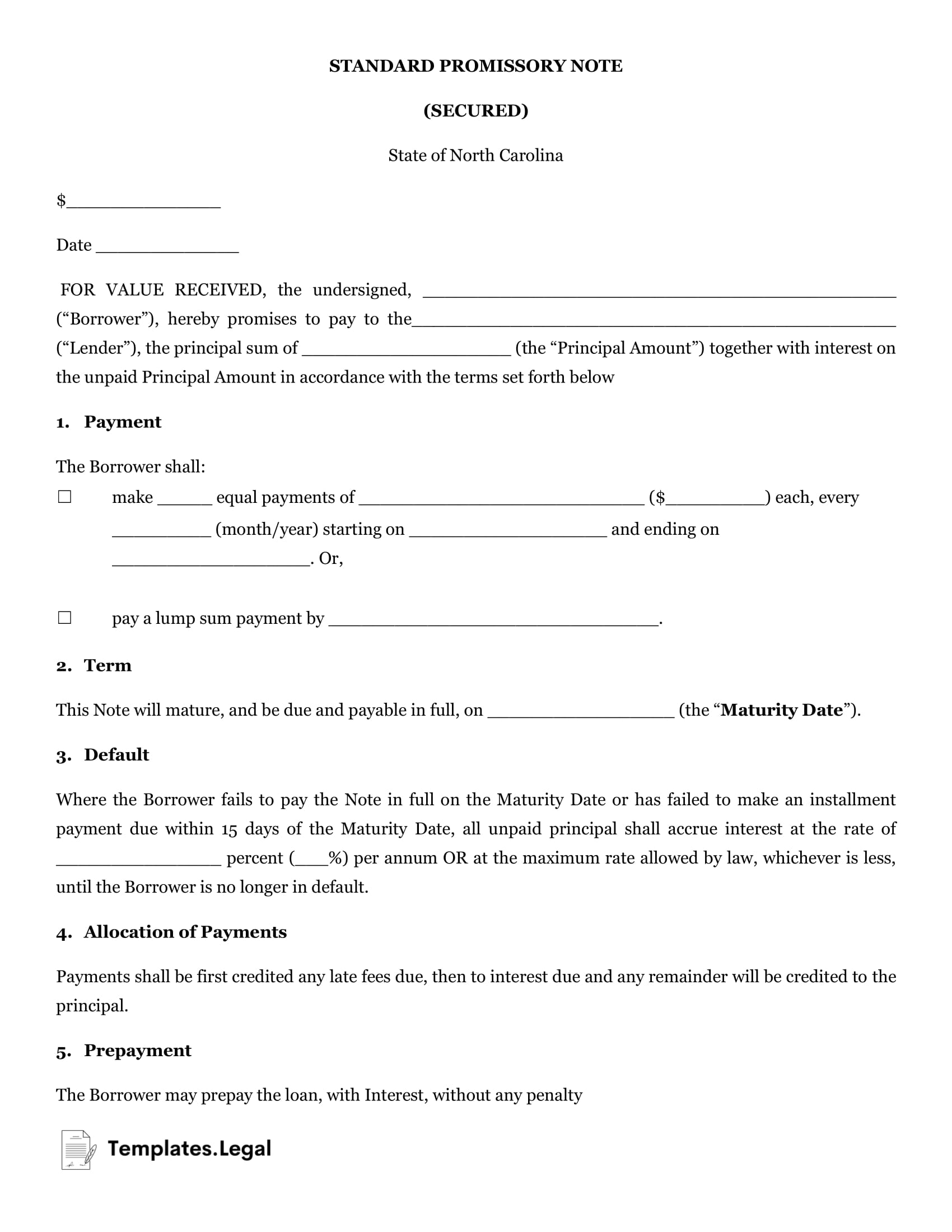

North Carolina Secured Promissory Note

In North Carolina, a secured promissory note protects the lender’s investment. The borrower must offer up a financially valuable collateral asset should they default on the loan. Secured promissory notes are common between parties without established trust, such as start-ups and investors.

The lender will receive compensation for the loan, even if it’s not in cash. The collateral doesn’t have to cover the entire amount of the loan, just the amount the borrower has to repay.

A promissory note template North Carolina will require the following information:

- Date of the loan agreement

- Borrower’s full name and address

- Lender’s full name and address

- The principal amount, or the loan value

- Interest rate, if any

- Loan repayment deadline

- How the borrower will repay the loan

- How many days may pass before the lender issues a late notice

- Signature of the borrower, lender, and perhaps a witness.

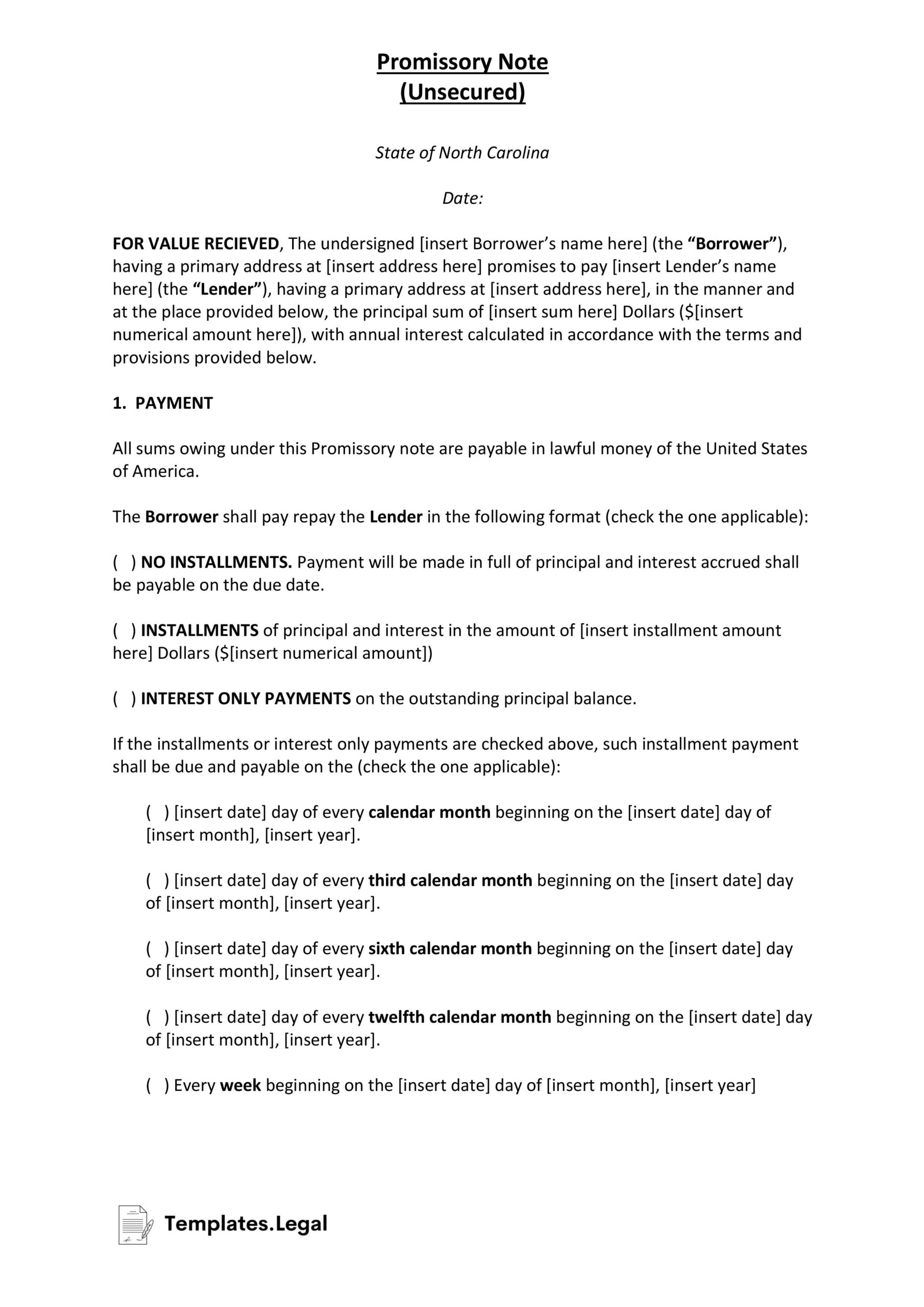

North Carolina Unsecured Promissory Note

Unsecured promissory notes do not require collateral should the borrower default on the loan. The lack of security means the note is riskier for the lender.

These notes are common between parties with a trusting relationship between them, such as long-term business partners, friends, or family members. Social capital is at stake instead of assets.

Even though these notes don’t use assets as collateral, a lender can take the promissory note North Carolina form and sue the borrower for the amount they didn’t pay. The lender would have to pay out of pocket or provide an asset to cover the remaining loan amount. Therefore, the lender can still receive reimbursement should the lender default on the loan.