South Carolina Promissory Note Templates

A South Carolina promissory note is a standard document that is legally binding. It requires that a borrower pay back any money that gets received from a lender.

Like most States, a South Carolina promissory note will stipulate a time frame for payment to take place as well as terms and conditions related to the loan. Other stipulations may follow as required by the South Carolina Code of Laws, with details outlined in the state’s Consumer Protection Code.

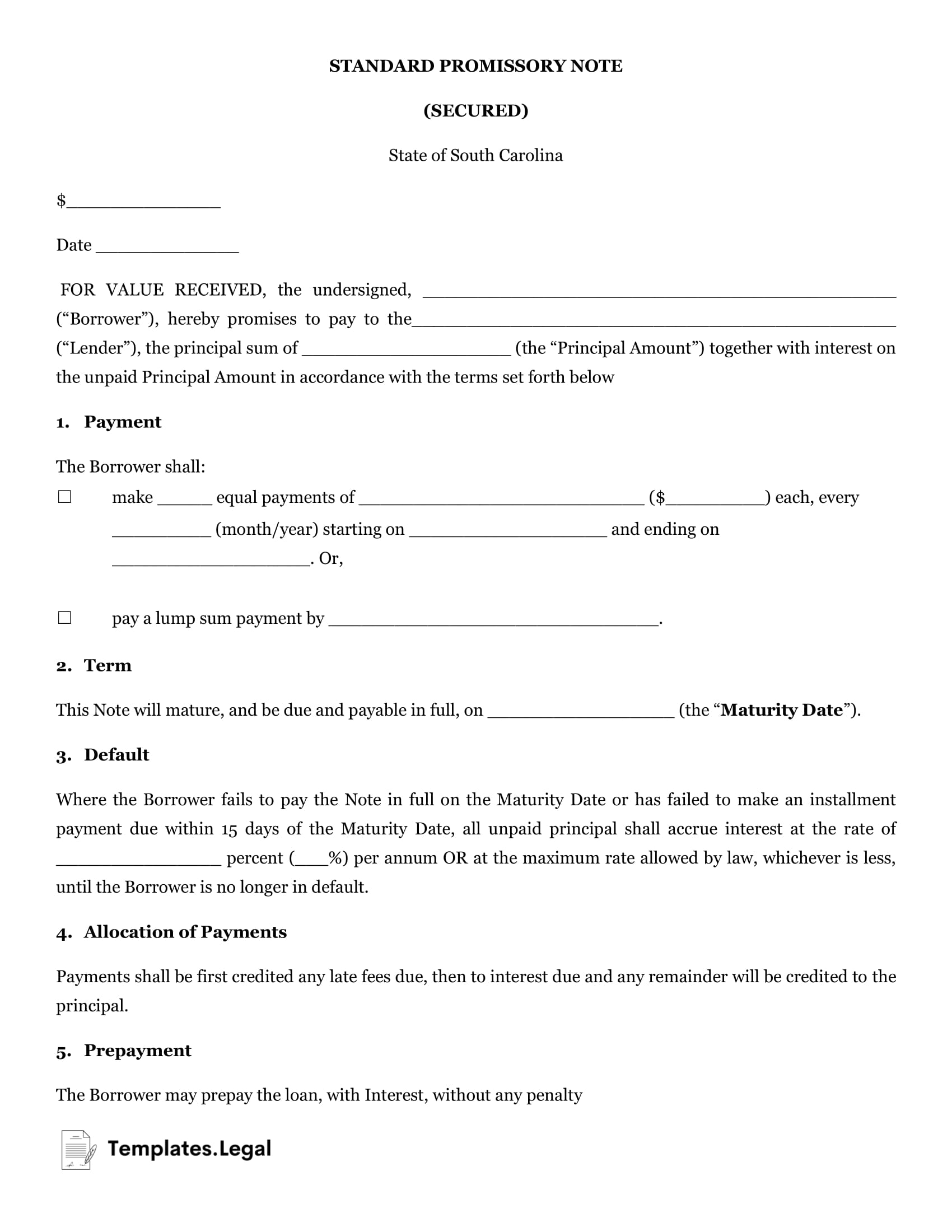

South Carolina Secured Promissory Note

A secured promissory note South Carolina form is an agreement made between the borrower and the lender in which the borrower agrees to put up collateral in case payment of the loan in not fulfilled.

Typically, secured promissory notes are needed for large loans, including personal loans made from banks and other lenders.

Interest rates will typically accompany the promissory note. In South Carolina, Title 34 of the South Carolina code of laws indicates that the interest rate depends on the amount of the loan and whether it is in writing.

When filling out a free South Carolina promissory note template, you will find it is straightforward. Components of the note include:

- Date of origination for the promissory note template South Carolina

- Names and addresses of the lender and borrower

- The loan amount, payments, and any information about collateral assets

- The due date and any accrued interest

- Any late fees and additional charges

- Additional information on any defaults of the loan or repayment

- Signatures by all parties

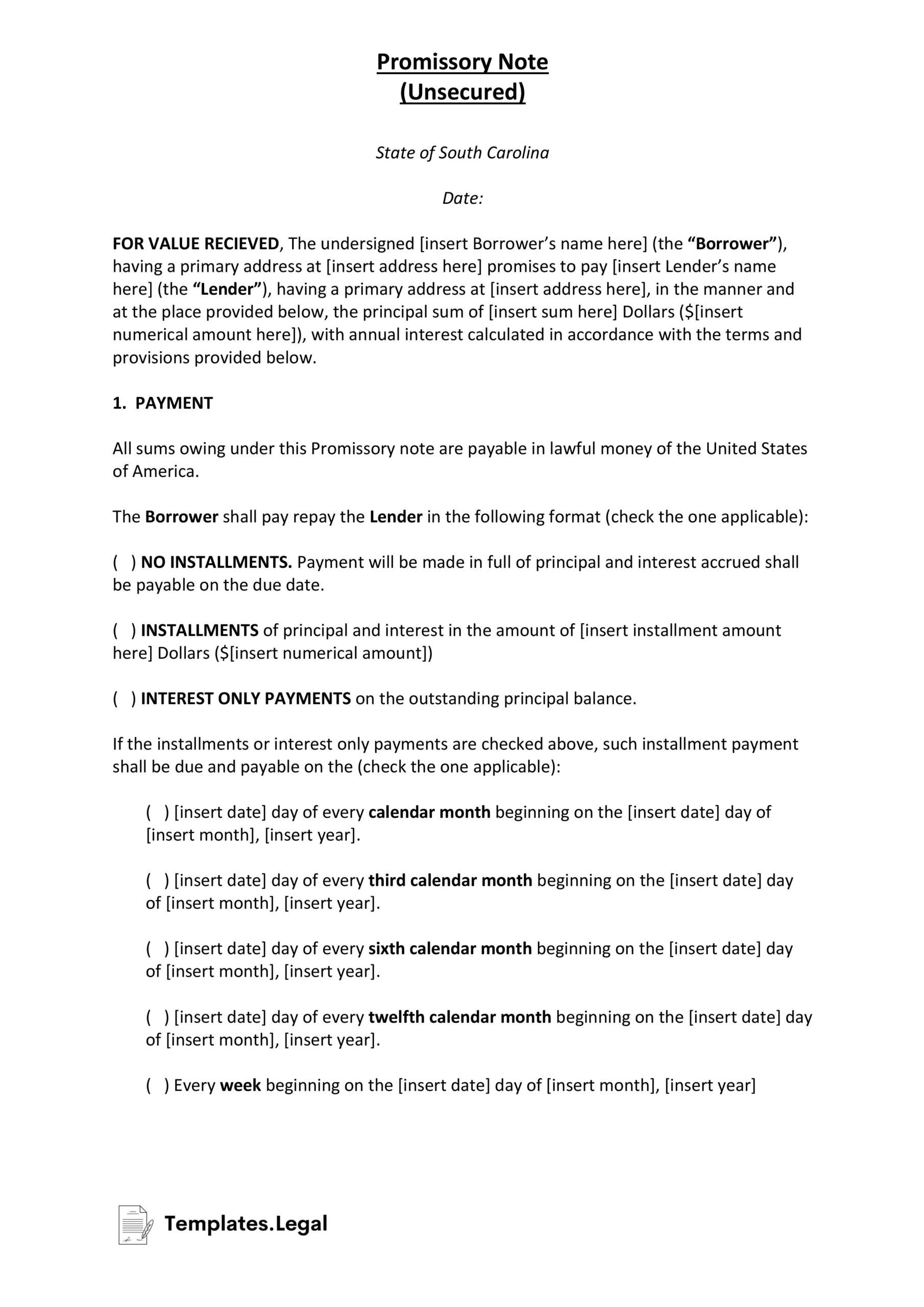

South Carolina Unsecured Promissory Note

Unlike a secured promissory note, South Carolina allows promissory notes to be drafted without the additional security of collateral. These notes are called unsecured promissory notes.

You will typically use an unsecured promissory note when drafting a repayment plan between friends and family. These types of loans will also be usually smaller in dollar amounts than secured promissory notes.

The drawback is that because these notes are unsecured, enforcing repayment or maintaining a strict repayment plan may be difficult.