Colorado Promissory Note Templates

To create a Colorado promissory note, you need to be aware of state-specific regulations that protect both the borrower and lender. A promissory note is an excellent tool for safeguarding the interest of moneylenders while also giving the borrower access to liquid capital.

It can be both “secured” (meaning, guaranteed by a valuable asset such as a vehicle or real estate), or “unsecured.” Since unsecured loans are inherently riskier propositions for the lender, they usually come with a higher interest rate.

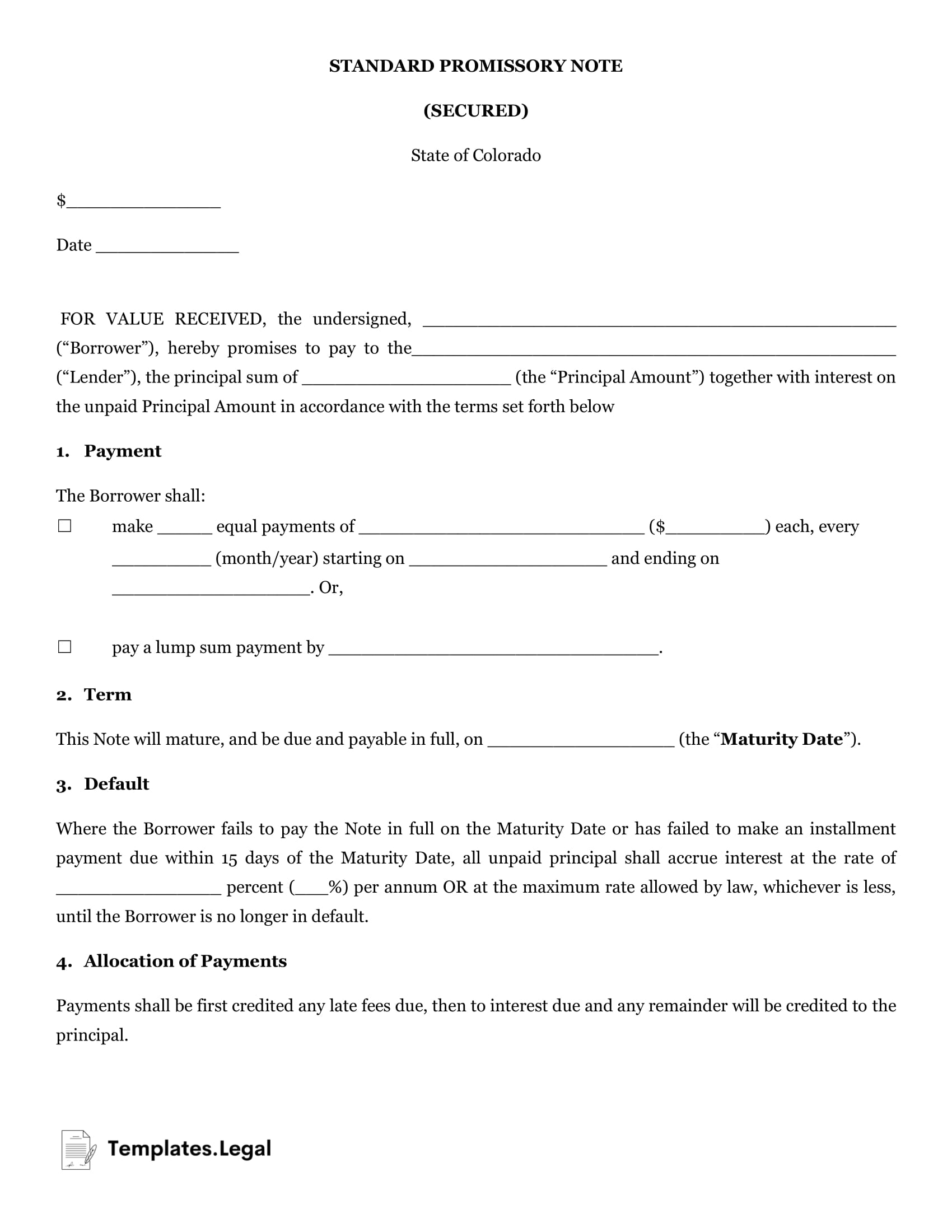

Colorado Secured Promissory Note

A secured promissory note guarantees that, in the event of a default, the lender will be made whole through repossession or transference of the borrower’s property. Secured promissory notes should always be accompanied by a security agreement which details the collateral that the borrower is putting up. Be as detailed as possible when describing the asset.

Here we’ve included a free Colorado promissory note template.

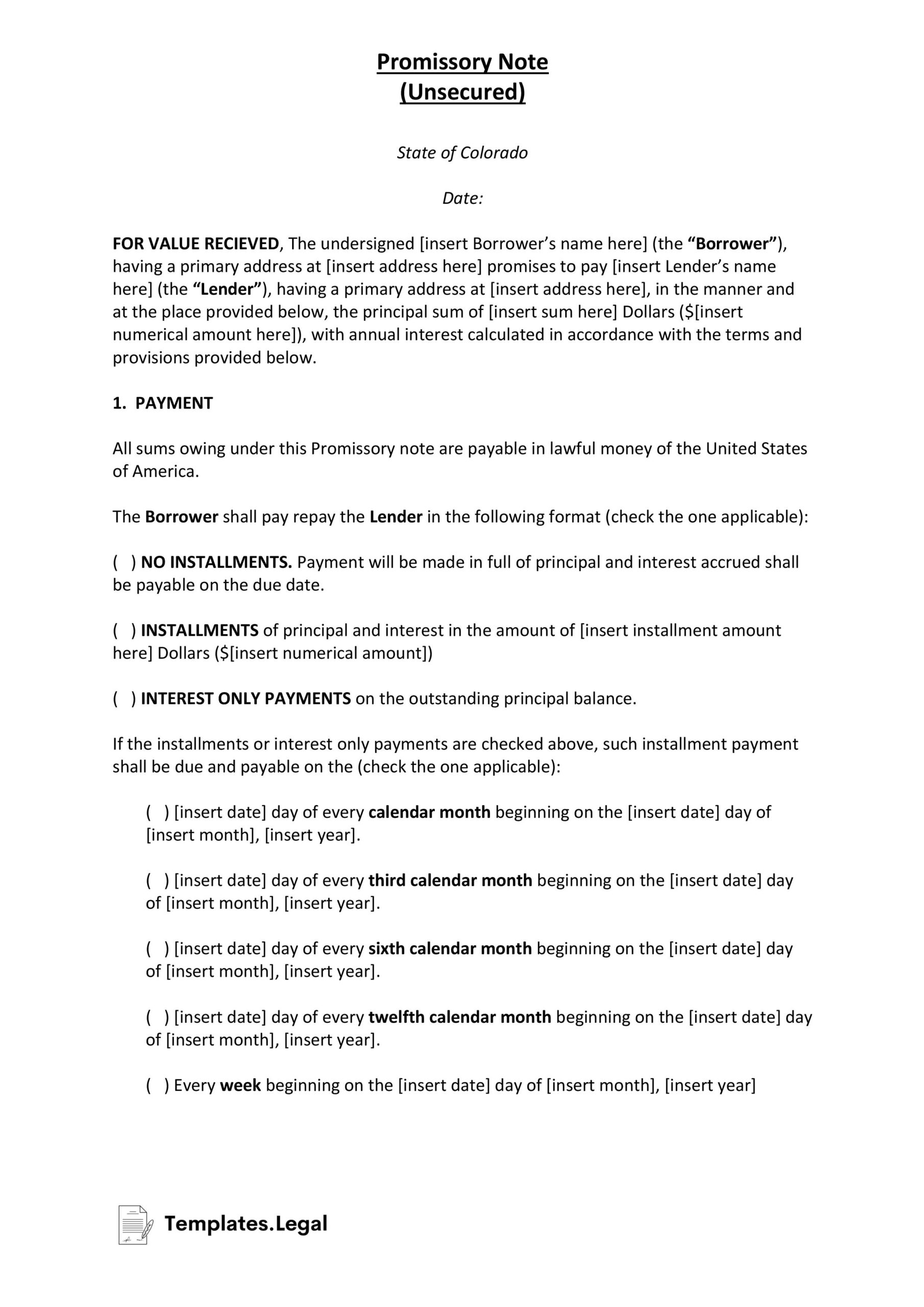

Colorado Unsecured Promissory Note

An unsecured promissory note comes with no guarantee that the lender will be made whole if the borrower cannot pay back the loan. Because of this risk, the lender usually charges a higher interest rate for the life of the loan, and typically requires an installment plan rather than one lump sum repayment.

Unsecured notes are normally seen with borrowers who have an excellent credit history or high income.

Colorado Promissory Note Regulations

One of the most important things to know before creating a Colorado promissory note form is your state’s usury laws. In Colorado, there are laws that prohibit the lender from charging exorbitant interest on a loan. The legal interest rate is 8% (in some cases 12%) when there is no physical document/agreement. This limit goes up to 45% when there is a document such as a Colorado promissory note.

If you opt for a secured promissory note, be aware that in Colorado, you are not permitted to collect on a healthcare insurance receivable or certain other general intangibles. Stick with physical property that is easy to repossess in the event of nonpayment.