Hawaii Promissory Note Templates

A Hawaii promissory note is a written agreement between two parties that memorializes the particulars of a loan. These two parties are known as the “borrower” and “lender.” Although in Hawaii, they are sometimes referred to as the “promissee” and “promissor.”

The agreement must outline critical details of the loan, such as interest rates, payment plans, and late fees.

Commercial promissory notes in Hawaii are subject to Article 3 of the Hawaii UCC (490:3) and Hawaii common law. Laws related to collections and interest rates also govern them.

Promissory notes in Hawaii can be either secured or unsecured.

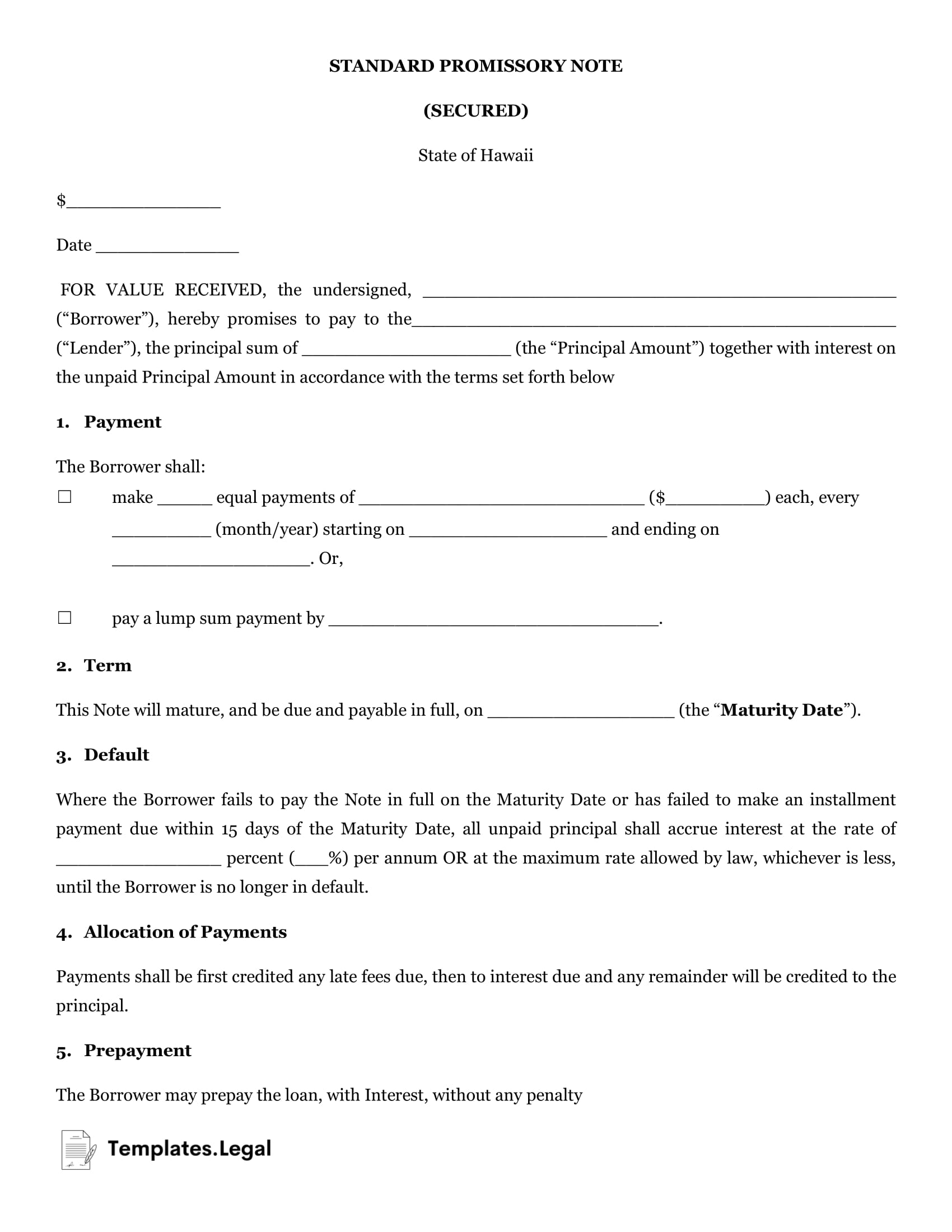

Hawaii Secured Promissory Note

A secured promissory note gives the lender the legal right to collect collateral from the borrower in case of nonpayment. The parties agree on the collateral before signing the loan, which is something of value, such as a car, home, or boat.

A secured promissory note should include the following information:

- The date

- The borrower and lender’s legal names and mailing addresses

- The principal amount loaned to the promissee

- Interest due

- The payment plan

- Description of the collateral

Additionally, the parties should include some clauses that define the agreement further. Some standard sections include things like prepayment, acceleration, attorney fees and costs, and payment allocation.

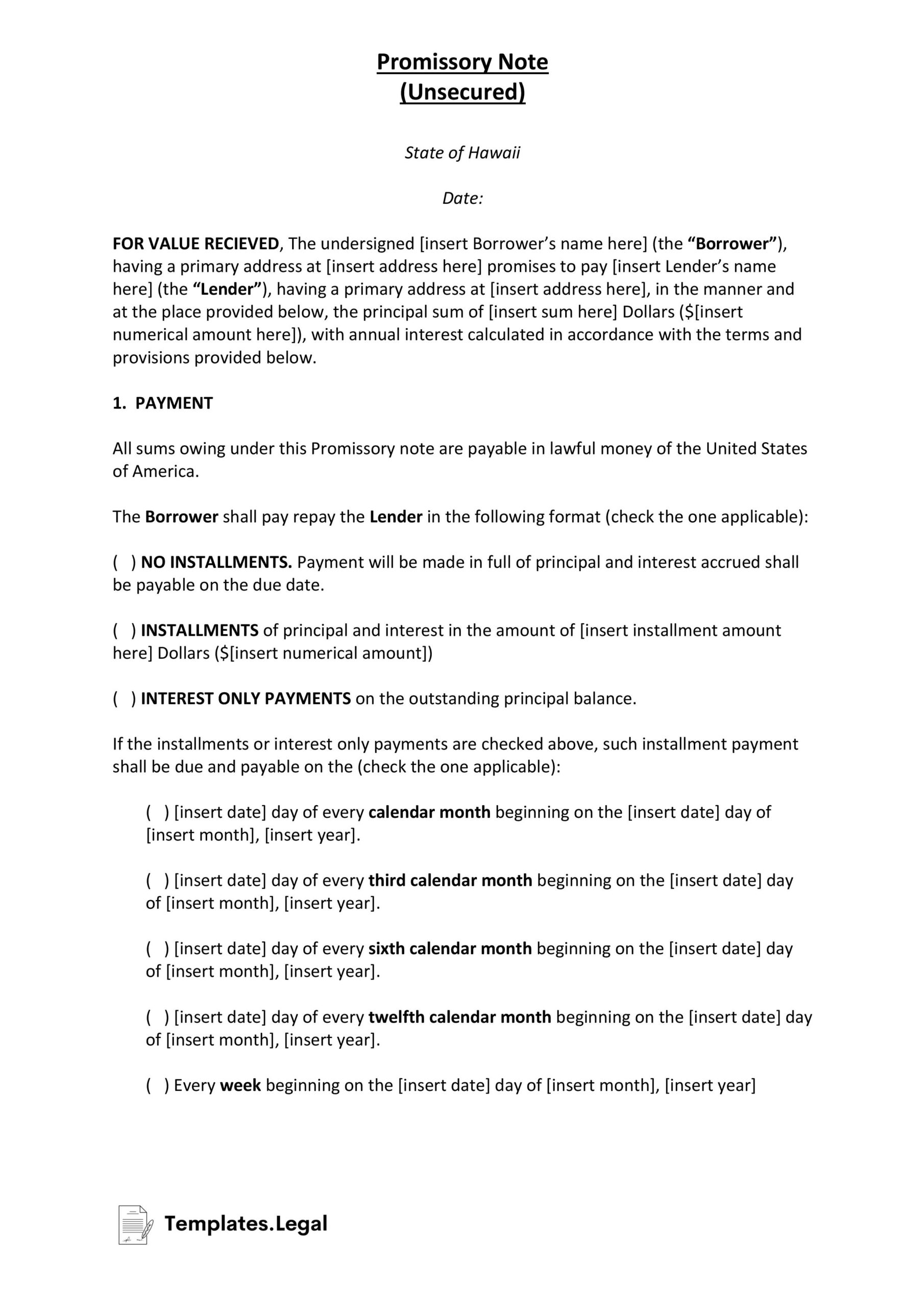

Hawaii Unsecured Promissory Note

An unsecured promissory note does not give the lender any guarantee in the form of collateral should the borrower default on the loan. Because they have no legal assurances, lenders using unsecured promissory notes should have full confidence in the borrower’s ability to repay them.

These types of agreements are common among family members and close friends. Individuals who have a high net worth or are otherwise considered trustworthy may be good candidates for this type of loan.

An unsecured loan agreement follows the same format as that of a secured loan. The only difference is that there is no mention of collateral.