Illinois Promissory Note Templates

An Illinois promissory note is a promise by a borrower to repay a loan. It must be signed by both the lender and the borrower. A promissory note outlines the terms of the loan. For example, certain parts of a promissory note may specify the amount of the loan and the period of time in which the loan should be paid in full. A promissory note in Illinois may be secured or unsecured.

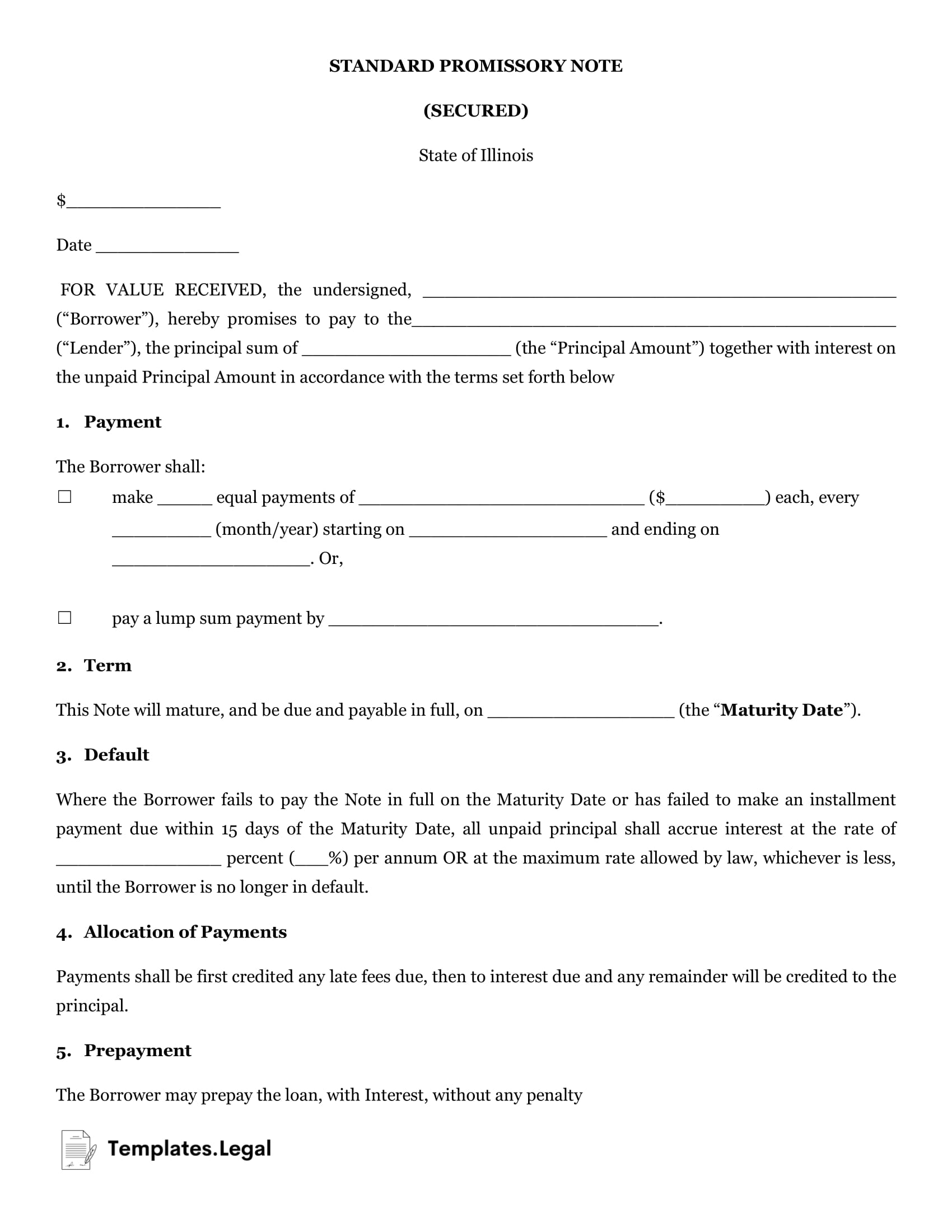

Illinois Secured Promissory Note

A secured promissory note allows the lender to secure a piece of the borrower’s property in the event the loan has defaulted. Common types of secured promissory notes include a car loan or mortgage. You need a promissory note Illinois form to denote the transaction.

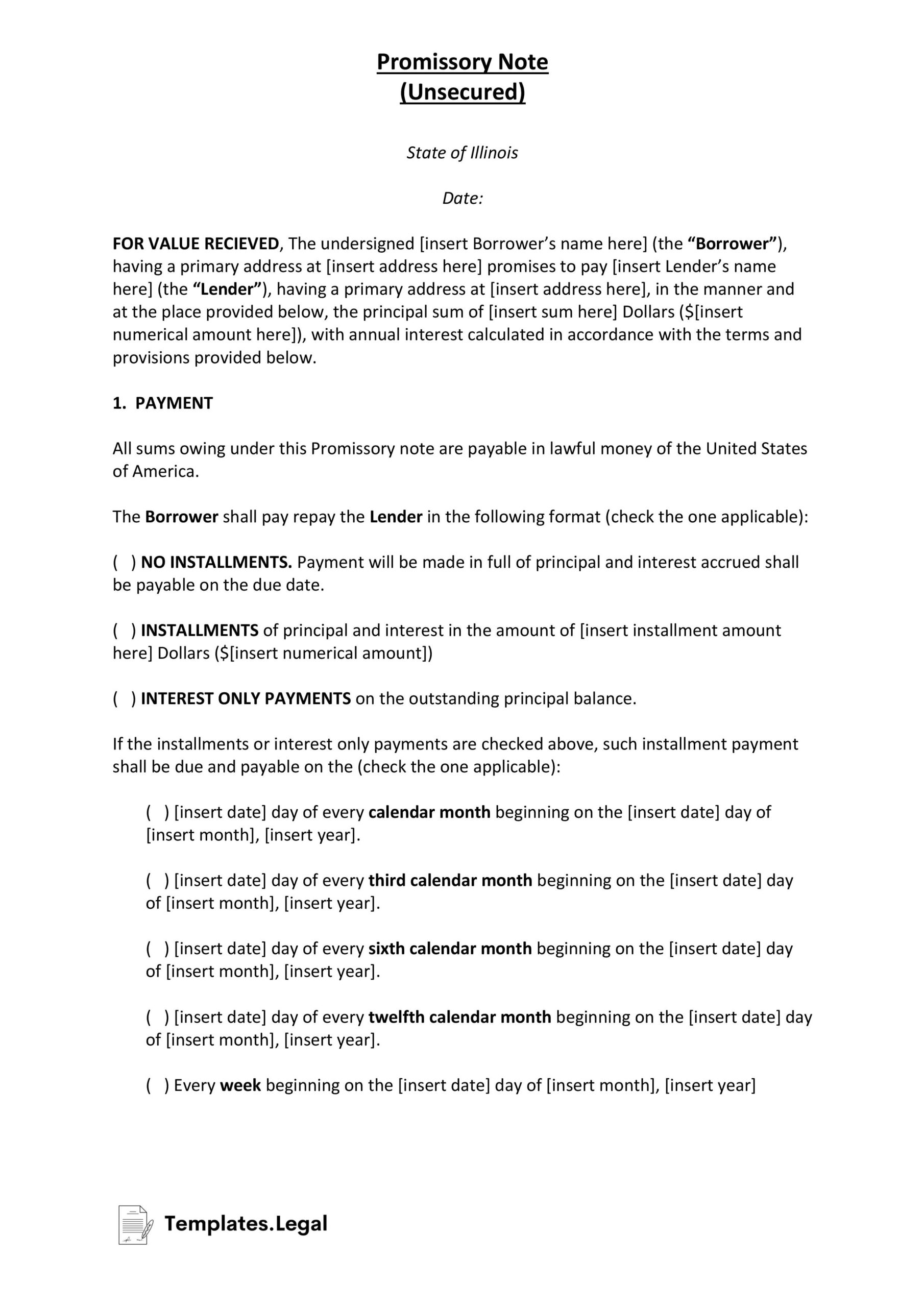

Illinois Unsecured Promissory Note

An unsecured promissory note doesn’t allow security if the debt is not paid in full. With unsecured promissory notes, the lender usually takes into account the borrower’s credibility without receiving anything in return. An unsecured promissory note template for Illinois can usually meet your needs. You can get a free Illinois promissory note online.