Maryland Promissory Note Templates

A Maryland promissory note is a type of loan agreement between a borrower and a lender. There might also be a co-signer who can be a third party to a promissory note.

In this agreement, the lender gives the borrower a loan and the borrower and co-signer — if there is one — acknowledge the terms and agree to repay the loan.

In the state of Maryland, there’s a legal interest rate (also known as a usury rate) of 6%, according to the state legislature.

There are two types of Maryland promissory notes: secured or unsecured.

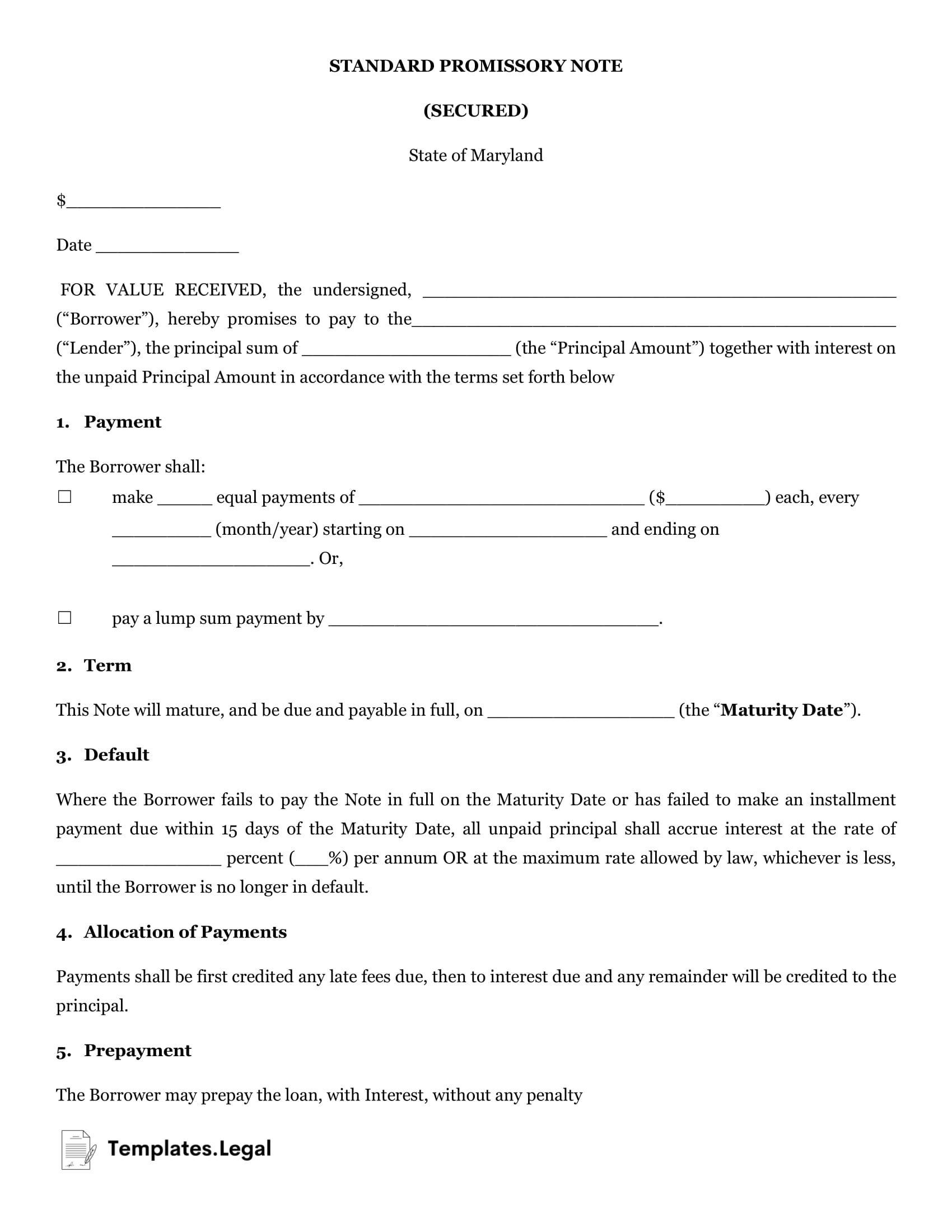

Maryland Secured Promissory Note

One version of a Maryland promissory note is referred to as a secured promissory note. It’s described as “secured” because the lender has more security with this type of agreement. Both parties — the lender and the borrower — agree on collateral that will be given to the lender if the borrower can’t repay the former. For example, a boat could be used as security.

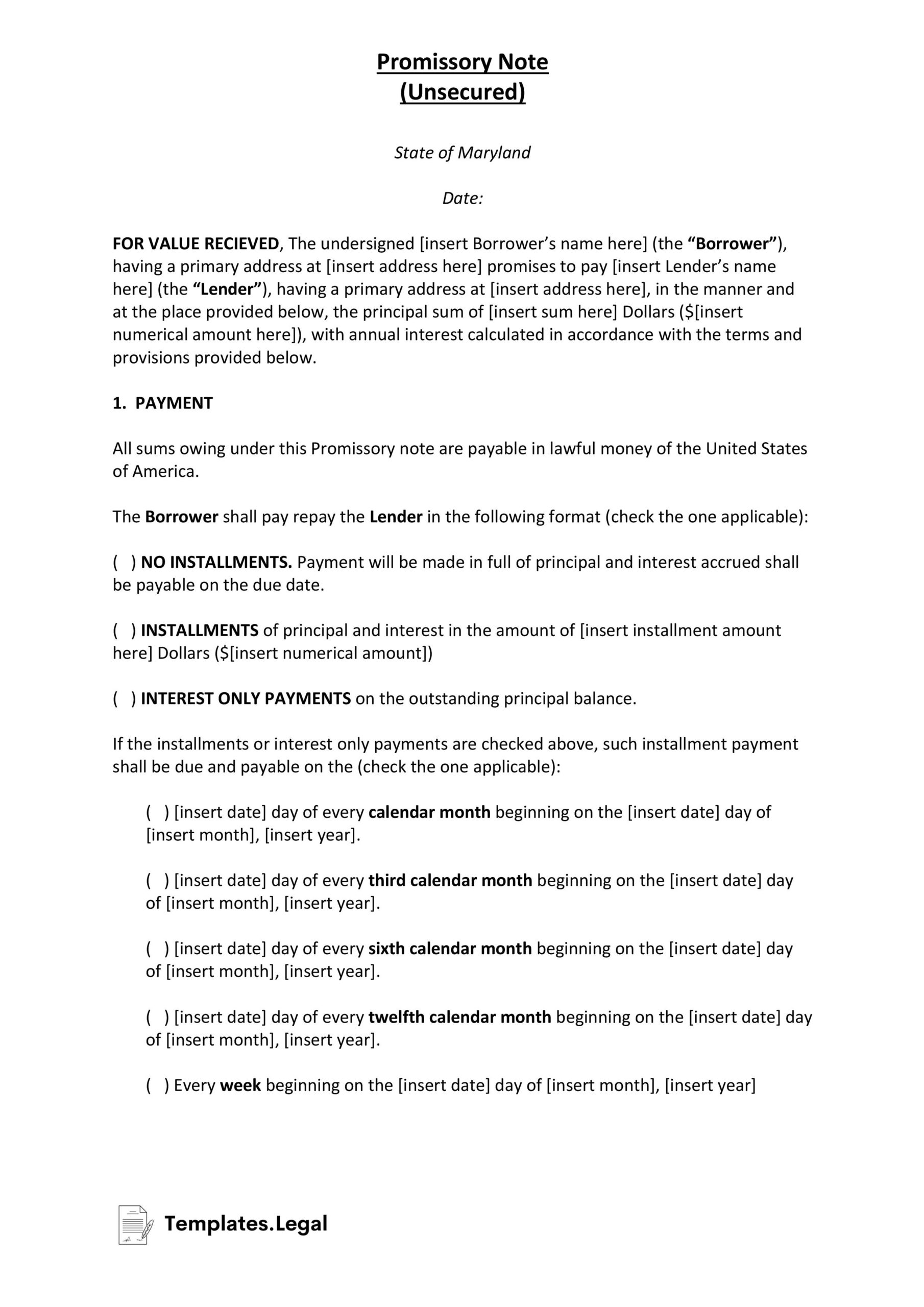

Maryland Unsecured Promissory Note

A free Maryland promissory note that’s unsecured puts the lender at risk of losing money because there’s no collateral offered. Lenders in this position should make sure the borrower has good credit. It also might be best to only use unsecured promissory note Maryland forms with trusted friends or family members.

A promissory note template for Maryland contains lots of important information. For example, this written agreement will include things like:

- The agreement date

- Who the borrower and lender are

- Payments and installments as well as the payment method

- Signatures