Unsecured Promissory Note Templates

Promissory notes are legal lending documents. They’re designed to help lenders secure payment from borrowers. A standard promissory note will state how much money the lender has loaned and expects repaid, and the amount of time the borrower has to repay that loan.

There are several different types and sub-types of promissory notes. Most of these notes are categorized by their purpose. For example, a borrower hoping to secure a car may create a vehicle promissory note.

Unsecured Promissory Note By State

Types of Promissory Notes

Promissory notes can be simple, personal, or intention-specific. Understanding the different types of promissory notes is vital to understanding the differences between secured and unsecured notes.

Simple Promissory Notes

Simple notes are straightforward agreements that do not require a listed purpose. A lender can provide a loan to a borrower and settle on the terms of repayment without having to specify what the loan will be used for.

Personal Promissory Notes

Personal notes are very similar to simple promissory notes. They are often used in transactions among family members or close friends. These documents primarily exist to provide documentation of personal loans, limiting the number of financial agreements concerning loans or repayment.

Other Types of Promissory Notes

There are several specific types of promissory notes, including investment notes, vehicle notes, student loan (master) promissory notes, commercial notes, and even real estate notes. Some of these types may require collateral, while others require very little information or security.

Still, promissory notes that are provided without an exchange of collateral are often considered to be unsecured. Nearly any type of promissory note can be unsecured, though the vast majority of unsecured promissory notes tend to be either simple or personal in nature.

What Is the Difference Between a Secured and Unsecured Promissory Note?

A secured promissory note is one that is backed by some type of collateral. Personal property and real estate are the two most widely accepted forms of collateral. If an individual is unable or unwilling to offer either of these forms of collateral when signing a promissory note, the result is an unsecured note.

If the borrower defaults on their payments to the lender, the lender can choose to use the note as evidence of a payment schedule and agreement while in court. That’s why most lenders will only pursue an unsecured note when working with credible individuals who are unlikely to default on their payments.

How to Create an Unsecured Promissory Note: Step-by-Step

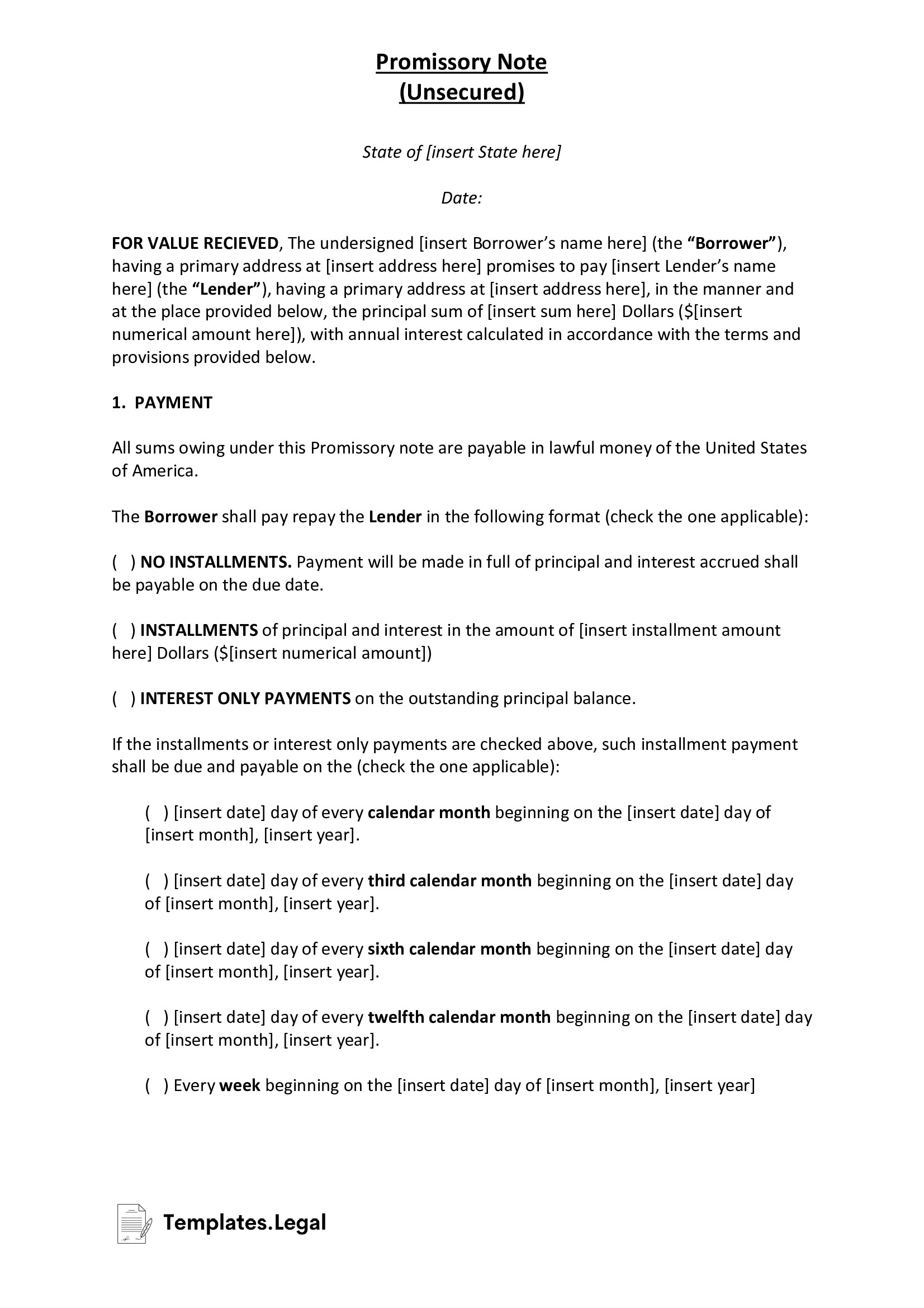

Creating an unsecured promissory note is slightly simpler than creating a secured one because there is zero collateral involved. All unsecured promissory notes contain the same depth of information. This information includes:

- A promise (on behalf of the lender) that the borrower will repay the loan or funds.

- The amount of the loan (including an applicable interest rate).

- A payment schedule and payment beneficiary (typically the beneficiary is the lender).

- The amount expected for each payment.

- A schedule of miscellaneous fees to be paid.

- A plan that outlines post-default actions, including the option to pursue legal action against the borrower.

Besides including this vital information, lenders or borrowers will want to ensure that their note is formatted and written correctly before submitting and signing it. In this instance, an unsecured note form or template may be helpful.

- Draft or Download an Unsecured Promissory Note Template

There are quite a few promissory note templates and forms accessible online that can save time while drafting a new note.

It’s important for the lender and borrower to discuss all of the required information listed above before signing any note. Once an agreement has been reached, both parties must formally state this agreement before moving forward. - Write the Terms of Agreement

The Terms of Agreement is typically placed at the top of a promissory note. Additional terms and information, such as the original principal loan amount and agreed-upon payment period, usually fall below this initial statement of agreement.

However, while it is crucial to include as much viable information in this section (and its related subsections) as possible, it’s equally important to ensure that you’ve gotten all the required signatures on this document/agreement. Without proper signature verification, a promissory note will not hold up in a court of law. - Ensure That All Signatures Are Present

Most notes require at least three signatures. The lender, the borrower, and an impartial witness or notary must all sign the agreement for it to have any legal standing. However, it may be wise to address the Right to Transfer Clause and the borrower’s Right to Cancel before obtaining these final, imperative signatures.

- Include a Right to Transfer Clause

The lender may want to transfer the borrower’s debt to another lender in the future, which is why they must inform the borrower of their right to transfer. The borrower should sign a statement that explains this clause and confirms that they understand what it entails. The same is true of the borrower’s right to cancel the note.

- Do Not Forget the Borrower’s Right to Cancel

Borrowers must sign beneath a statement that explains their right to cancel the note within three days of signing. This right does not allow borrowers to gain access to funds, then decide to cancel their promise to repay those funds. Instead, it simply offers borrowers the chance to change their minds before the lender supplies the loan.

Frequently Asked Questions

Below you will find answers to some of the most frequently asked questions regarding unsecured promissory notes. Should you fail to find the answer to your question, do not hesitate to contact a local attorney or lawyer for legal advice and assistance.

Conclusion

Unsecured promissory notes are more beneficial to borrowers than they are to lenders. That’s because an unsecured note does not involve any collateral. If a borrower defaults on their payments to the lender, it is the responsibility of the lender to seek legal action against the borrower.

This process can be expensive and time-consuming, which is why most lenders will only agree to draft an unsecured note if the borrower has excellent credit and a lengthy history of on-time payments.